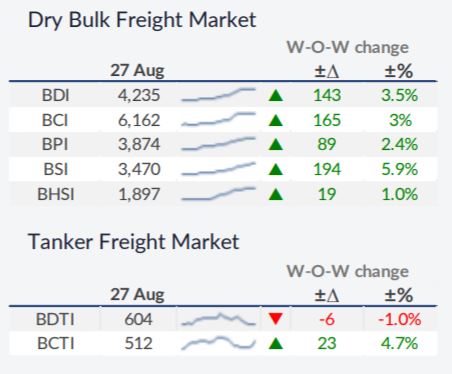

The dry bulk market has completed a remarkable summer and as we head towards the end of 2021, market delegates are trying to determine whether it can take the next step forward or not? In its latest weekly report, shipbroker Allied Shipbroking said that “of little surprise has been the fact that the dry bulk market has closed off the summer period on a positive tone, given the further boost in freight rates noted during the month of August. Being relatively close to the final quarter of the year, now is as good time as any to look in depth at the underlining statistics, as well as the dynamics and momentum noted in the spot market”.

Source: Allied Shipbroking

According to Allied, “the final quarter is typically a point where many look to debate whether we are about to see the next big step or not. Year-to-date the rally in realized earnings has put the overall sector on a completely different trajectory. That comes hand-to-hand with the overall sentiment at such bullish terms not seen for many years. Notwithstanding this, it seems somehow excessive to think that the current situation is a “new era” for shipping markets, especially when given the current pandemic situation where everything is in a state of constant change and there are still many unknowns at hand”.

Source: Allied Shipbroking

Allied’s Thomas Chasapis, Research Analyst, said that “at this point, current freight rate levels are closer to those noted back in 2010. Choosing 2010 as a base year could help us better understand both the historical change in trends as well as the relative performance across the different size segments. Undoubtedly, the Capesize market is the underperformer. It may well have hit the US$ 50,000/day mark right now, however it still lags in terms of yearly average and max figure, when compared with that of 2010. Nevertheless, this gap may well quickly close if we were to see a “typical” firm 4Q that this segment “enjoys” from time to time. In the Panamaxes, things seem rather on par with that noted in 2010. At this point, the “hidden” gems have mostly been the smaller size segments. This year both the Supramax and Handysize segments have outperformed their respective performance of 2010, while indicating stronger momentum and dynamics, as measured by different metrics such as average, percentile, and max figures”.

Chasapis added that “forward sentiment has also experienced a huge leap, given the impressive recovery in asset prices, period TC rates and FFA figures since the start of the year. For the bigger size segment, year-to-date average growth has been in the region of 56% for closing figures of FFA contracts with duration period calendar years 2022 and 2023. Moreover, the next 7-year average as presented in the paper market is close to US$ 17,000/ day, well above the actual average returns of the past 7-years. However, excluding the negative shock in the spot market during late 2015 and 2016, forward sentiment doesn’t veer far from its long-term average.

Source: Allied Shipbroking

In other size segments, the FFA bull-run on a year-to-date basis has been even more impressive. As we shift to smaller sizes, the closing numbers for the next 2-years has almost doubled, while the forward view for the next 7-year period has limited to any connection with what the spot market has actually done in previous years. For Panamaxes, Supramaxes and Handysizes, the gap between the spot market’s average returns in 2014-2020 and forward returns (as depicted by FFAs) for 2022-2028, is close to US$ 5,000/day. The dry bulk market has taken an asymmetrically bullish stance for the next couple of years or so, as shown by the period TC and FFA markets. For the time being, this seems attuned with the overall trend in spot freight earnings, as well, asset price levels. However, given the level of uncertainty prevailing in the market, could it be that all this bullish stance being expressed as to the market’s future dates be misleading given the level of risk that these hold?”, Allied’s analyst concluded.

Nikos Roussanoglou, Hellenic Shipping News Worldwide