Dynagas LNG Partners LP, an owner and operator of liquefied natural gas (“LNG”) carriers, announced its results for the three and six months ended June 30, 2021.

Second Quarter Highlights:

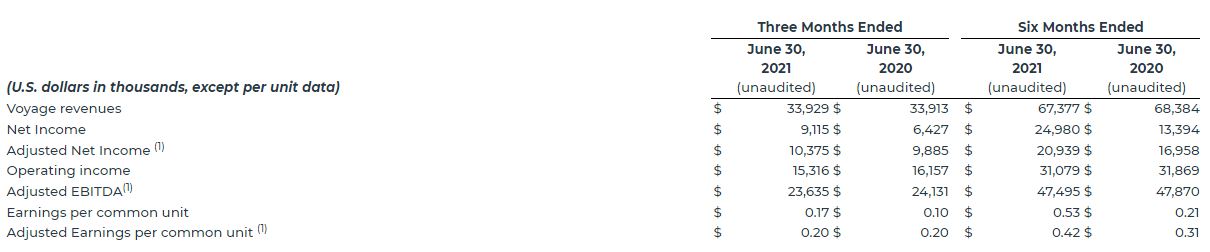

• Net income and earnings per common unit of $9.1 million and $0.17, respectively;

• Adjusted Net Income(1)of $10.4 million and Adjusted Earnings per common unit of $0.20;

• Adjusted EBITDA(1) $23.6 million;

• 100% fleet utilization(2);

• Declared and paid cash distribution of $0.5625 per unit on its Series A Preferred Units (NYSE: “DLNG PR A”) for the period from February 12, 2021 to May 11, 2021 and $0.546875 per unit on the Series B Preferred Units (NYSE: “DLNG PR B”) for the period from February 22, 2021 to May 21, 2021;

• Sold $2.15 million of common units at an average price per unit of $2.8769 pursuant to the Partnership’s Amended & Restated Sales Agreement, which had $26.5 million of remaining availability as of June 30, 2021; and

• Entered into a new time charter party agreement with Equinor ASA (“Equinor”) for the employment of our LNG carrier Arctic Aurora. Under the new time charter agreement, the Arctic Aurora is expected to be delivered to Equinor in September 2021 in direct continuation of the current charter party with Equinor, meaning there will be no lapse of time between the current and the new time charter. The term ‘in direct continuation’ does not refer to the contracted income.

Subsequent Events:

• Declared a quarterly cash distribution of $0.5625 on the Series A Preferred Units for the period from May 12, 2021 to August 11, 2021, which was paid on August 12, 2021 to all preferred Series A unit holders of record as of August 5, 2021;

• Declared a quarterly cash distribution of $0.546875 on the Series B Preferred Units for the period from May 22, 2021 to August 21, 2021, which was paid on August 23, 2021 to all preferred Series B unit holders of record as of August 16, 2021.

1) Adjusted EBITDA, Adjusted Net Income, and Adjusted Earnings per common unit are not recognized measures under U.S. GAAP. Please refer to Appendix B of this press release for the definitions and reconciliation of these measures to the most directly comparable financial measures calculated and presented in accordance with U.S. GAAP and other related information.

(2) Please refer to Appendix B.

CEO Commentary:

We are pleased to report the results for the three months period ended June 30, 2021.

All six LNG carriers in our fleet are operating under their respective long-term charters with international gas producers with an average remaining contract term of 7.4 years.

As of September 7, 2021, our estimated contracted revenue backlog is approximately $1.09 billion. We were pleased to announce on April 21, 2021 a new two-year charter for the Arctic Aurora with Equinor, which has had the ice classed 1A and winterized vessel on continuous charter since her delivery from builders in 2013. After securing the charter for the Arctic Aurora with Equinor, and barring any unforeseen events, the earliest contracted re-delivery date for any of our six LNG carriers is in the third quarter of 2023 (the Arctic Aurora), with the next carrier (the Clean Energy) becoming available for re-chartering in the first quarter of 2026.

For the second quarter of 2021, we reported Net Income of $9.1 million, earnings per common unit of $0.17, Adjusted Net Income of $10.4 million, Adjusted Earnings per common unit of $0.20 and Adjusted EBITDA of $23.6 million.

The COVID19 outbreak is still causing operational and logistical challenges for the industry. Despite these challenges, we are pleased to report 100% utilization for our fleet for the second quarter of 2021.

Going forward, we intend to continue our strategy of using our cash flow generation to deleverage our balance sheet and reinforce our liquidity so as to build equity value over time. This, we believe, will enhance our ability to pursue future growth initiatives.

Financial Results Overview:

Adjusted Net Income, Adjusted EBITDA, and Adjusted Earnings per common unit are not recognized measures under U.S. GAAP. Please refer to Appendix B of this press release for the definitions and reconciliation of these measures to the most directly comparable financial measures calculated and presented in accordance with U.S. GAAP.

Three Months Ended June 30, 2021 and 2020 Financial Results

Net Income for the three months ended June 30, 2021 was $9.1 million as compared to a Net Income of $6.4 million in the corresponding period in 2020, which represents an increase of $2.7 million, or 42.2%. This increase was mainly attributable to the decrease in finance costs as well as to the decrease in loss on our interest rate swap transaction entered into in May 2020, which were slightly offset by the increase in operating and general and administrative expenses as compared to the corresponding period in 2020.

Adjusted Net Income for the three months ended June 30, 2021 was $10.4 million compared to $9.9 million in the corresponding period in 2020, representing a net increase of $0.5 million or 5.1%, mainly due to the net effect of the decrease in finance costs and the increase in operating and general and administrative expenses as compared to the corresponding period in 2020.

Voyage revenues for both the three months ended June 30, 2021 and the three months ended June 30, 2020 were $33.9 million.

The Partnership reported average daily hire gross of commissions(1) of approximately $62,440 per day per vessel in the three-month period ended June 30, 2021, compared to approximately $62,200 per day per vessel in the corresponding period in 2020. During both three-month periods ended June 30, 2021 and 2020, the Partnership’s vessels operated at 100% utilization.

Vessel operating expenses were $7.6 million, which corresponds to daily operating expenses per vessel of $13,945 in the three-month period ended June 30, 2021, as compared to $6.9 million, or daily operating expenses per vessel of $12,630 in the corresponding period in 2020. This increase is mainly attributable to higher crewing and supply costs in the three-month period ended June 30, 2021 as compared to the corresponding period in 2020, due to the effects of the outbreak of the Covid-19 pandemic.

Adjusted EBITDA for the three months ended June 30, 2021 was $23.6 million, as compared to $24.1 million for the corresponding period in 2020. The decrease of $0.5 million, or 2.1%, was mainly due to the increase in operating and general and administrative expenses as explained above.

Interest and finance costs, net, were $5.4 million in the three months ended June 30, 2021 as compared to $6.3 million in the corresponding period in 2020, which represents a decrease of $0.9 million, or 14.3% due to the lower weighted average interest and the reduction in the average interest bearing debt as compared to the corresponding period in 2020.

For the three months ended June 30, 2021, the Partnership reported Earnings per common unit and Adjusted Earnings per common unit, basic and diluted, of $0.17 and $0.20 respectively, after taking into account the distributions relating to the Series A Preferred Units and the Series B Preferred Units on the Partnership’s Net income/Adjusted Net Income. Earnings per common unit and Adjusted Earnings per common unit, basic and diluted, are calculated on the basis of a weighted average number of 36,661,237 common units outstanding during the period and in the case of Adjusted Earnings per common unit after reflecting the impact of the non-cash items presented in Appendix B of this press release.

Adjusted Net Income, Adjusted EBITDA and Adjusted Earnings per common unit are not recognized measures under U.S. GAAP. Please refer to Appendix B of this press release for the definitions and reconciliation of these measures to the most directly comparable financial measures calculated and presented in accordance with U.S. GAAP.

Amounts relating to variations in period–on–period comparisons shown in this section are derived from the condensed financials presented below.

(1) Average daily hire gross of commissions represents voyage revenue excluding the non-cash time charter deferred revenue amortization, divided by the Available Days in the Partnership’s fleet as described in Appendix B.

Liquidity/ Financing/ Cash Flow Coverage

During the three months ended June 30, 2021, the Partnership generated net cash from operating activities of $15.8 million as compared to $8.1 million in the corresponding period in 2020, which represents an increase of $7.7 million, or 95.1%.

As of June 30, 2021, the Partnership reported total cash of $86.8 million (including $50.0 million of restricted cash). The Partnership’s outstanding indebtedness as of June 30, 2021 under the $675.0 Million Credit Facility amounted to $591.0 million, gross of unamortized deferred loan fees and including $48.0 million, which were repayable within one year.

During the three months ended June 30, 2021, the Partnership sold $2.15 million of common units at an average price per unit of $2.8769 pursuant to the amended and restated ATM Sales Agreement entered into in August 2020, for the offer and sale of common units representing limited partnership interests, having an aggregate offering amount of up to $30.0 million (the “Current ATM Program”). Following these sales, the Current ATM Program had $26.5 million of remaining availability and the Partnership has 36,802,247 units issued and outstanding, as of June 30, 2021.

As of June 30, 2021, the Partnership had unused availability of $30.0 million under its interest free $30.0 million revolving credit facility with its Sponsor, or the $30.0 Million Revolving Credit Facility, which was extended on November 14, 2018, and is available to the Partnership at any time until November 2023.

Vessel Employment

As of September 7, 2021, the Partnership had estimated contracted time charter coverage(1) for 100% of its fleet estimated Available Days (as defined in Appendix B) for 2021, 100% of its fleet estimated Available Days for 2022 and 95% of its fleet estimated Available Days for 2023.

As of the same date, the Partnership’s estimated contracted revenue backlog (2) (3) was $1.09 billion, with an average remaining contract term of 7.4 years.

(1) Estimated Time charter coverage for the Partnership’s fleet is calculated by dividing the fleet contracted days on the basis of the earliest estimated delivery and redelivery dates prescribed in the Partnership’s current time charter contracts, net of scheduled class survey repairs by the number of expected Available Days during that period. Actual time charter coverage may vary.

(2) The Partnership calculates its estimated contracted revenue backlog by multiplying the contractual daily hire rate by the expected number of days committed under the contracts (assuming earliest delivery and redelivery and excluding options to extend), assuming full utilization. The actual amount of revenues earned and the actual periods during which revenues are earned may differ from the amounts and periods disclosed due to, for example, dry-docking and/or special survey downtime, maintenance projects, off-hire downtime and other factors that result in lower revenues than the Partnership’s average contract backlog per day.

(3) $0.15 billion of the revenue backlog estimate relates to the estimated portion of the hire contained in certain time charter contracts with Yamal which represents the operating expenses of the respective vessels and is subject to yearly adjustments on the basis of the actual operating costs incurred within each year. The actual amount of revenues earned in respect of such variable hire rate may therefore differ from the amounts included in the revenue backlog estimate due to the yearly variations in the respective vessels’ operating costs.

Source: Dynagas LNG Partners LP