Global demand for high-grade nickel, an essential component in electric vehicle (EV) batteries, will outweigh supply by 2024. An analysis by Rystad Energy indicates that although global supply will continue its steady year-on-year climb, rising demand spurred in part by the energy transition will lead to a shortage in less than two years.

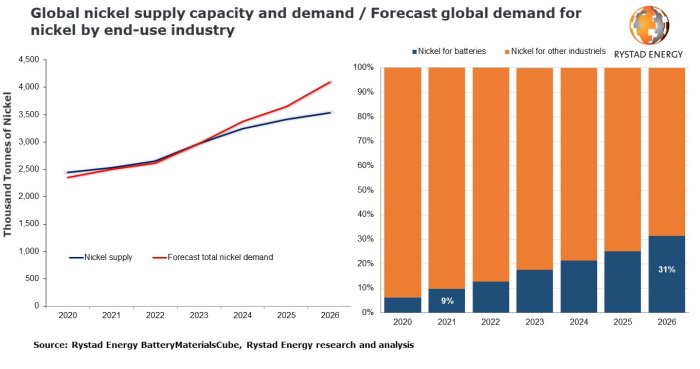

Global nickel demand is forecast to climb to 3.4 million tonnes (Mt) in 2024 from 2.5 Mt this year. Rystad Energy’s analysis of existing mines, projects and development plans estimates that global supply will fall short of demand in 2024, with production of 3.2 Mt. The gap between global supply and demand will then widen quickly to a deficit of 0.56 Mt by 2026.

Nickel is an essential component of the batteries used by many automakers, and a supply shortage could cause numerous headaches and ripples across Western car manufacturing. In addition, the deficit is likely to encourage automakers to assess alternative battery chemistries, as well as search for previously untapped nickel deposits.

“The potential nickel shortage could encourage industry leaders to look to previously unattractive sources of nickel, including deposits in Indonesia. However, the process of extracting nickel from these deposits has inherent risks and challenges, including environmental, social and governance (ESG) concerns,” says James Ley, global energy metals expert and Senior Vice President with Rystad Energy.

“The shortage has no other obvious solution in sight that won’t tarnish carmakers with several unattractive ESG issues. Therefore, we expect Western EV manufacturers to explore alternative battery options as the nickel procurement problem becomes increasingly difficult,” Ley adds.

What’s driving the supply crunch?

The battery market is growing in leaps and bounds, spurred by the electrification of the global fleet of passenger cars. Rystad Energy expects nickel-based battery chemistries to hold the largest share of the market by 2030, slightly ahead of iron-based batteries, with other solutions trailing far behind these two main groups.

Limited access to nickel could throw a spanner in the wheels of this forecast, however, as the battery industry has to compete for supply with other growing industries, such as steelmaking.

Unlike other essential battery raw materials used for cathodes such as lithium, the battery market is not the dominant end-user for nickel in the short term. According to our estimates, the stainless-steel industry accounts for more than 70% of current global nickel demand, with the battery market making up less than 10% of global nickel metal demand in 2020.

Nickel metal demand from the stainless-steel industry is expected to grow at about 5% per year, while the market for batteries is poised to explode. In an unconstrained supply scenario, batteries could require more than 1 Mt of nickel metal by 2030, quadrupling from the current demand of 0.25 Mt.

The battery market only accounts for 9% of the current global supply of about 2.3 Mt, but forecasts show its market share could rise to 31% by 2026. This surging demand from the battery market will place huge pressure on the nickel supply chain in less than a decade.

Mining companies are not finding enough new high-grade nickel deposits to keep up with battery production demands. As a result, automakers and battery manufacturers may seek alternative battery chemistries to meet demand.

What’s the solution?

The primary nickel-based battery chemistries are nickel manganese cobalt (NMC) and nickel cobalt aluminum (NCA), while the iron-based chemistries are lithium iron phosphate (LFP) and sodium-ion (Na-ion). Nickel-intensive batteries are the batteries of choice of many Western manufacturers due to their high energy density combined with a lower proportion of cobalt. Cobalt is mainly mined in the Democratic Republic of Congo, where poor ESG credentials make it unattractive for car manufacturers.

Because of the uncertainty and risk of battery-grade nickel supply in the coming decade, automakers may seek to decrease their dependency on nickel and instead opt for lithium iron phosphate batteries, where nickel is not required, for certain models or geographies. For example, this year, both Volkswagen and Tesla have announced plans to use LFP batteries in their lower-end vehicles as the energy density of these batteries has improved enough to make them suited for electric cars. This will help reduce the companies’ long-term concerns over nickel supply and could prove a fruitful path forward for other EV manufacturers.

For more analysis, insights and reports, clients and non-clients can apply for access to Rystad Energy’s Free Solutions and get a taste of our data and analytics universe.

Source: Rystad Energy