[ad_1]

Capacity along the Asia has continued to increase throughout 2021, despite several setbacks, including a canal blockage, container shortages, and port congestion.

Container rates on the Asia to North Europe have skyrocketed over the course of the year. The Freightos Baltic Index (FBX) has reached $13,118 as of the week July 16, the highest it’s been during the year.

Congestion at Northern European ports and Asian ports have raised issues for carriers. Yantian has recently experienced a coronavirus outbreak which caused delays and limited handling capabilities. Antwerp has been experiencing delays as well. Maersk indicated that delays at Antwerp could reach 3 to 5 days at their MPET/PSA terminal. MSC announced they shifted calls to Antwerp on their Maersk-partnered 2M Alliance “Griffin” service to Le Havre for 6 weeks, as initially reported.

Despite these issues, capacity has remained tight and has been increasing steadily throughout the year.

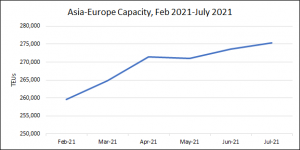

The BlueWater Reporting’s Capacity Report shows the estimated allocated weekly TEUs raising from 259,611 TEUs on the last week of February to 275,344 TEUs as of the latest week of this July, a 6 percent increase. The only dip was from April to May, 271,502 TEUs to 270,965 TEUs respectively.

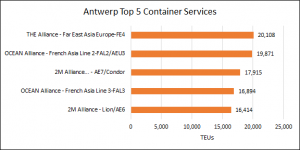

The top five container services calling Antwerp following their omission on the “Griffin” service, based off the average vessel size in TEUs, are listed in the chart above. The top service is THE Alliance’s “FE4” service with 20,108 TEUs. Each of the services are carrier alliance service and along the Asia to Europe trade route, indicating the reliance of trade from Asia is for Antwerp.

Source: Douglas Kingston, BlueWater Reporting

[ad_2]

This article has been posted as is from Source