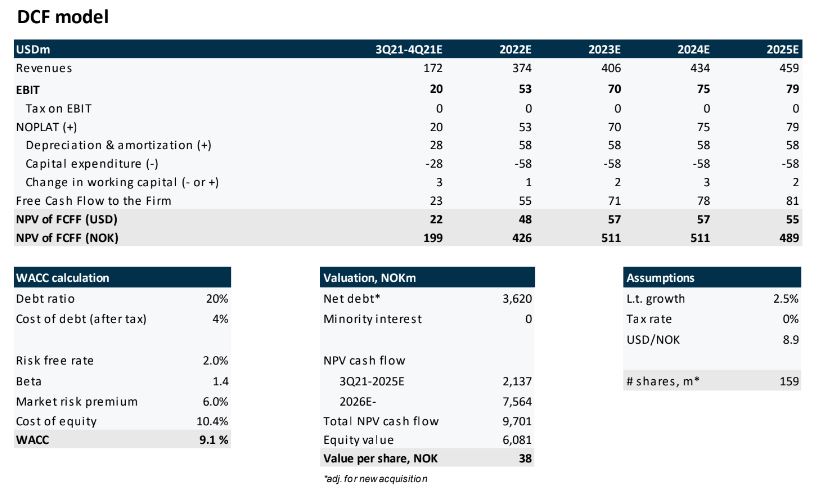

BW Epic Kosan posted 2Q21 results this morning with higher than we predicted revenues, but somewhat lower EBITDA due to increased operating expenses. Still, the bottom line remained in a positive territory. Also, just yesterday it was announced about the addition of two vessels to the fleet. As the long-term outlook remains unchanged and positive, we will make limited changes to the estimates and our positive stance towards the stock is likely to be reiterated.

Increased OPEX and SG&A costs

Very solid revenues figure of USD 81.5m beat our expectations of USD 74.2m, but the increased expenses brought the EBITDA figure below our projections. The growth of underlying OPEX were explained by the change in the fleet mix to include the more-expensive-to-operate semi-refrigerated and ethylene vessels and by Covid-19, which were primarily related to crew change expenses and freight forwarding costs for spares. SG&A expenses increased due to costs incurred during the combination with BW Kosan and should reduce in the future. Still, the bottom line came in a positive territory at USD 3.3m (USD 7.3m expected).

Two more vessels acquired

Yesterday it was announced, that BW Epic Kosan acquired two 9,000 LPG/ammonia/ethylene capable carriers built in 2008 from Odfjell SE. This, when finalized, would increase the number of ethylene carriers to 21 (in addition to 48 pressurized and 9 semi-refs).

Demand/supply still encouraging; more focus on IMO targets

For the balance of 2021 the challenges of 2020 are expected to remain. However, the longer-term fundamentals remain strong, with expected LPG seaborne trade growth significantly beating the smaller gas vessel fleet growth forecasts even before scrapping. Also, the company communicated on the increased focus towards IMO 2030 and 2050 targets. BWEK is working not only on reduction of CO2, but also on projects that support wider decarbonization, such as shipping related to carbon capture and storage. Many of the vessels were said to be capable of carriage of future clean fuels, including ammonia.

This was the first full quarter after joining the forces with BW Kosan. Despite significantly increased expenses, the bottom line remained in a positive territory and as the long-term fundamentals stay strong, we are likely to make limited changes to our estimates.

Source: Norne Research