The dry bulk market is expected to post additional gains in the weeks to come, thanks to a growing list of positive fundamentals. In its latest weekly report, shipbroker Intermodal said that “the strong freight performance since the beginning of year has continued for the dry bulk market with earnings being at the highest level in over a decade. As a result, vessels’ values have improved substantially, whilst demolition activity has stalled over the past two months. Older ships are attracting a lot of SnP interest at levels substantially above their scrap values. On top of this, the dry bulk orderbook continues to hover at low levels, as yards’ slots are filled with orders on other more profitable sectors, namely containers”.

According to Intermodal’s SnP Broker, Mr. Vasilis Moiris, “China has been the primary driving force behind the market improvement, as steel production has been running at record high levels, while demand for grains has accelerated owing to the better trade relationships with USA and the pig herd recovery from African Swine Fever which previously had a substantial impact in the specific trade.

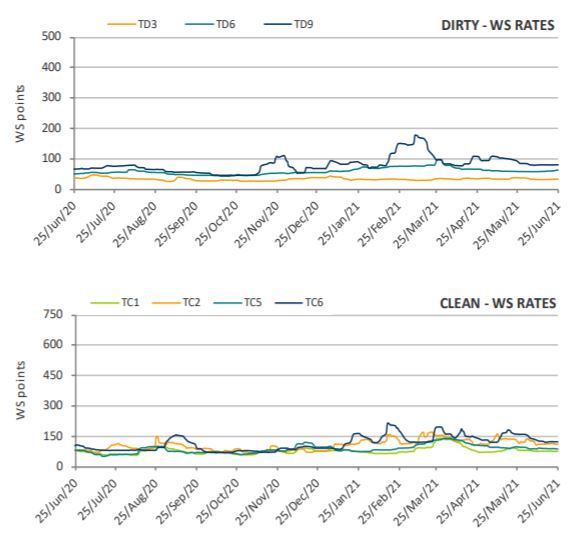

Source: Intermodal

What is more, commodities demand from the rest of the world is accelerating and intensifying trade inefficiencies in favor of dry bulk trade i.e. international steel prices are at record high levels, West-East steel price arbitrages, industrial output growth globally driving demand for iron ore and coking coal and a projected above average hot summer is seeing Europe and Asia competing for thermal coal. Minor bulks demand is also upbeat and sustains the upward freight trend for the geared dry bulk segment. The commodities price rally is in the meantime incentivizing more production and exports by miners, in order to take advantage of high prices, thus market players expect seaborne volumes to increase further in the coming months”.

The shipbroker added that “increased trade has resulted in port congestion mounting to multi year highs; Port congestion in the Pacific is also supporting the supply side in the short term mainly in the Panamax sector whilst it is expected to have a positive impact on Capesize as well. The freight market picture has been positively reflected into asset values. It is not though that the larger sizes have shadowed the geared ships, as in comparison geared vessels and Panamax in sequence have so far performed better in proportion to their value than a Capesize. Nonetheless, current FFA levels are supporting a further improvement in the spot market for Capesize during the second half of the year. If the spot market catches up pace with period earnings suggested by FFA levels as market participants anticipate, we should expect SnP interest to increase in the next quarters for the largest size and asset values to appreciate in tandem”, Moiris concluded.

Nikos Roussanoglou, Hellenic Shipping News Worldwide