Global Ship Lease, Inc., an owner of containerships, announced its unaudited results for the three and six month periods ended June 30, 2021.

Second Quarter 2021 and Year To Date Highlights

– Reported operating revenue of $82.9 million for the second quarter 2021. Operating revenue for the six months ended June 30, 2021, was $155.9 million.

– Reported net income available to common shareholders of $30.1 million for the second quarter 2021 after $7.8 million net gain from sale of the 2,272 TEU 2001 built, containership, La Tour and a prepayment fee of $1.4 million on the completion of the refinancing of our Deutsche, CIT, HCOB, Entrust, Blue Ocean Credit Facility (“Odyssia Credit Facilities”), giving normalized net income(3) for the quarter of $23.7 million.

– For the six months ended June 30, 2021, net income available to common shareholders was $34.2 million, after $5.8 million premium paid on the full optional redemption of our outstanding 9.875% Senior Secured Notes due 2022 (“2022 Notes”) on January 20, 2021, an associated non-cash write off of deferred financing charges of $3.7 million and of original issue discount of $1.1 million, a non-cash charge of $1.3 million for accelerated stock based compensation expense, a prepayment fee of $1.6 million on the partial repayment of the Blue Ocean Junior Credit Facility, the prepayment fee of $1.4 million on the completion of the refinancing of our Odyssia Credit Facilities and the $7.8 million net gain from sale of La Tour, giving normalized net income(3) for the six months of $41.5 million.

– Generated $51.5 million of Adjusted EBITDA(3) for the second quarter 2021. Adjusted EBITDA for the six months ended June 30, 2021 was $96.2 million.

– Earnings per share for the second quarter of 2021 was $0.83. Earnings per share for the six months ended June 30, 2021 was $1.00.

– Declared a dividend of $0.25 per Class A common share for the second quarter of 2021 to be paid on September 3, 2021 to common shareholders as of August 23, 2021. Paid a dividend of $0.25 per Class A common share for the first quarter 2021 on June 3, 2021 to common shareholders of record as of May 24, 2021, more than double the $0.12 per Class A common share announced on January 12, 2021, as a result of fleet growth and success in rechartering.

– During the second quarter 2021, raised $23.6 million net proceeds under the ATM program for the 8.75% Series B Preferred Shares (“Series B Preferred Shares”). During the period from July 1, 2021 through August 4, 2021, a further $6.4 million net proceeds was raised under this ATM program. Since the inception of this ATM program a total of $60.8 million net proceeds has been raised.

– During the second quarter 2021, raised a further $7.6 million net proceeds under the ATM program for the 8.00% Senior Unsecured Notes due 2024 (“2024 Notes”). The total outstanding 2024 Notes as at June 30, 2021 was $117.5 million, which includes the issuance of $35.0 million of the 2024 Notes to the sellers of 12 vessels, as part of the consideration. Since the inception of this ATM program a total of $50.9 million net proceeds has been raised.

– During the period from April 1, 2021 through August 4, 2021, took delivery of seven 6,000 TEU Post-Panamax containerships purchased for an aggregate price of $116.0 million, and chartered them back to Maersk Line, as announced in the press release of February 9, 2021. In April 2021, entered into a new credit facility with HCOB for six of these seven ships and drew down all tranches of $10.7 million each, amounting to a total of $64.2 million. One tranche was drawn down in July. The seventh vessel was financed by a sale and leaseback agreement with Neptune for $14.7 million.

– On April 13, 2021, Kelso and Maas Capital sold an aggregate of 5,175,000 Class A common shares in an underwritten public offering at $12.50 per share. Our free float increased, although we did not receive any proceeds from the sale of these Class A common shares.

– On April 16, 2021, drew down in full on a new $51.7 million secured credit facility to refinance one of the three existing tranches of the Odyssia Credit Facilities that had a maturity date on June 30, 2022. The second tranche was refinanced on May 7, 2021 with a new $51.7 million secured credit facility. The third tranche was refinanced on May 27, 2021, with a new $54.0 million sale and leaseback agreement with CMBFL.

– On June 8, 2021, announced agreement to purchase from Borealis Finance LLC, 12 containerships with an average size of approximately 3,000 TEU and a weighted average age of 11 years for an aggregate purchase price of $233.9 million. All 12 vessels were delivered between July 15 and July 29, 2021. In July 2021, entered into a new syndicated credit facility with HCOB and Credit Agricole for a total of $140.0 million to part finance the purchase price. The remaining purchase price was financed by cash on hand and the issuance of $35.0 million of our existing 2024 Notes to the sellers of the ships.

– On June 16, 2021, announced agreement to purchase four 5,470 TEU ultra-high reefer capacity Panamax containerships with an average age of approximately 11 years for an aggregate purchase price of $148.0 million. On delivery, the ships will be chartered to a leading liner operator for a firm period of three years each, with a charterer’s option for a period of an additional three years. The ships are scheduled for delivery during the third and fourth quarter of 2021. The purchase price is expected to be covered by cash on hand and new senior secured debt.

– On June 30, 2021, sold the 2,272 TEU 2001 built, La Tour, for net proceeds of $16.5 million resulting in a net gain of $7.8 million.

– On July 12, 2021, Moody’s upgraded the Corporate Family Rating to B1 / Stable from B2 / Positive.

– Between January 1 and August 4, 2021, including the charters on the 23 ships we have either purchased or contracted to purchase year to date, we have added 40 charters (including extensions), representing approximately $906 million of contracted revenues and $662 million of expected aggregate Adjusted EBITDA – calculated on the basis of the median firm periods of the respective charters. 18 charters were for 1,100 – 3,500 TEU feeder ships, eight were for 4,250 – 5,470 TEU Panamax ships, and 14 were for 5,900 – 6,800 TEU Post-Panamaxes. Charter durations ranged from approximately 21 months to five years, with shorter durations for the smaller ships and longer durations for the larger ships. Rates were up significantly against those previously contracted.

George Youroukos, Executive Chairman of Global Ship Lease, stated, “Moving into the summer months, the containership charter market has continued to reach new heights, driven by strong underlying containerized trade and an ongoing tightness in the supply of ships. These strong fundamentals, combined with continued port congestion and a generally overburdened logistics supply chain, have resulted in effectively full employment of the global fleet, which has, in turn, driven charter rates to record highs and has led to extended charter durations, now several times what they have been throughout the last decade. Looking forward, we are very encouraged to see a highly constrained supply of containerships through at least 2023/2024, particularly in the mid-sized asset classes where we focus, and a prospective long tail of containership demand supported by both high consumer demand for imported goods and anticipated restocking simply to restore retail inventories to more normalized levels. We also factor in the tougher environmental regulations that are set to come into effect starting in January 2023. Compliance with these new regulations will not only have a positive environmental impact by reducing emissions, but will also require much of the global containership fleet to slow down substantially, thus reducing effective capacity, with a one knot reduction in speed equating to a reduction of approximately 5-6% in fleet capacity.”

“Against this backdrop, we have remained very active in acquiring high-quality containerships with strong return profiles and minimal downside risk. Already in 2021, we have grown our fleet by over 50% while adding over $900 million of contracted revenues and over $660 million of contracted estimated Adjusted EBITDA. Our ability to continuously engage in immediately accretive growth throughout the mid-sized and smaller vessel classes, and to unlock the full potential of vessels with best-in-class reefer capacity, has proven the strength and scalability of the Global Ship Lease platform while also dramatically expanding our earnings and contracted revenues. Even as we continue to grow by taking delivery of recently acquired vessels and pursuing further such acquisitions as meet our criteria, we also expect to realize meaningful earnings growth in the coming months as a number of our ships renew charters in the hottest market in recent memory. This combination of highly supportive fundamentals, a proven strategy, and clear visibility on both contracted cashflows and attractive growth opportunities puts GSL in a strong position to continue generating excellent returns and ensuring a reliable and appealing dividend for our shareholders.”

Ian Webber, Chief Executive Officer of Global Ship Lease, commented, “In tandem with the commercial success that we have achieved, with new multi-year charters ensuring that we will benefit from the current market strength well into the future, we have continually seized opportunities to optimize our balance sheet and improve our long-term financial strength. In the first seven months of 2021, by the full redemption of our restrictive 2022 Senior Secured Notes and our other refinancing initiatives, we have refinanced $377.2 million of debt, removing all material maturities through end 2022, and dramatically improved our debt service and amortization profile while reducing our blended cost of debt from 6.3% to 5.2%. With the enhanced financial capabilities provided by these improved borrowing terms and affirmed by a further credit rating upgrade from Moody’s early in the third quarter, we remain continually active to ensure that the true strength and long-term prospects of our business are fully reflected throughout our balance sheet and capital structure.”

SELECTED FINANCIAL DATA – UNAUDITED

(1) Operating Revenue is net of address commissions which represents a discount provided directly to a charterer based on a fixed percentage of the agreed upon charter rate. Brokerage commissions are included in “Time charter and voyage expenses”.

(2) Net Income available to common shareholders.

(3) Adjusted EBITDA and Normalized Net Income are non-U.S. Generally Accepted Accounting Principles (“U.S. GAAP”) financial measures, as explained further in this press release, and are considered by Global Ship Lease to be a useful measure of its performance. For reconciliations of these non-U.S. GAAP financial measure to net income, the most directly comparable U.S. GAAP financial measure, please see “Reconciliation of Non-U.S. GAAP Financial Measures” below.

Revenue and Utilization

Revenue from fixed-rate, mainly long-term, time-charters was $82.9 million in the three months ended June 30, 2021, up $11.5 million (or 16.1%) on revenue of $71.4 million for the prior year period. The increase in revenue is principally due to (i) a 3.9% increase in ownership days, due to the addition of six vessels during the second quarter 2021, to 4,255 in the quarter, compared to 4,095 in the second quarter 2020 (ii) a reduction in planned offhire days from 210 in the second quarter of 2020 to 168, (iii) increased revenue on charter renewals at higher rates from Maira, Nikolas, Dolphin II, Athena, Orca I, Ian H, GSL Ningbo and Julie, partially offset by decreases in revenue on renewals at lower rates from Maira XL, CMA CGM Alcazar, CMA CGM Chateau d’If and MSC Tianjin and, (iv) less idle time, down to 12 days in the second quarter 2021 from 194 in the second quarter 2020 mainly due to GSL Matisse and Utrillo which were held for sale as at June 30, 2020 and were sold in July 2020. The 168 days of offhire for dry dockings in the second quarter 2021 were attributable to five regulatory dry-docking. With 12 days idle time and 36 days of unplanned offhire days, utilization for the second quarter 2021 was 94.9%. In the comparative period of 2020, the 210 days of offhire for dry-dockings were mainly attributable to three dry-dockings in progress as of June 30, 2020, one for regulatory reasons and two for scrubber installation on Agios Dimitrios and MSC Qingdao. With 161 days idle time for GSL Matisse and Utrillo prior to their sale, 33 idle days for Julie and GSL Christen between charters and 20 days of unplanned offhire days, utilization was 89.6%.

For the six months ended June 30, 2021, revenue was $155.9 million, up $13.6 million (or 9.6%) on revenue of $142.3 million in the comparative period, mainly due to the factors noted above.

The table below shows fleet utilization for the three and six months ended June 30, 2021 and 2020, and for the years ended December 31, 2020, 2019, 2018 and 2017.

Two dry-dockings for regulatory requirements were completed in the quarter and as of June 30, 2021, three such dry-docking were in progress. In 2021, we anticipate eight further dry dockings for the existing fleet.

Vessel Operating Expenses

Vessel operating expenses, which primarily include costs of crew, lubricating oil, repairs, maintenance, insurance and technical management fees, were up 16.1% to $28.1 million for the second quarter 2021, compared to $24.2 million in the comparative period. The increase of $3.9 million was mainly due to 160 or 3.9% net additional ownership days in the second quarter 2021 as a result of the acquisition and delivery of six vessels since April 1, 2021, all of which are Post-Panamax with on average higher daily operating expenses, offset by the disposal of GSL Matisse and Utrillo in July 2020 and due to crew replacement and delivery of spares which were significantly reduced in prior year periods as a result of COVID-19 restrictions and delays. The average cost per ownership day in the quarter was $6,609, compared to $5,902 for the prior year period, up $707 per day, or 12.0%.

For the six months ended June 30, 2021, vessel operating expenses were $52.4 million, or an average of $6,450 per day, compared to $49.7 million in the comparative period, or $6,125 per day, an increase of $325 per ownership day, or 5.3%.

Time Charter and Voyage Expenses

Time charter and voyage expenses comprise mainly commission paid to ship brokers, the cost of bunker fuel for owner’s account when a ship is off-hire or idle and miscellaneous owner’s costs associated with a ship’s voyage. Time charter and voyage expenses were $2.1 million for the second quarter 2021, compared to $2.7 million in the second quarter of 2020. The decrease is mainly due to the decrease in idle days and unplanned off hire days resulting in lower costs for bunker fuel for owner’s account.

For the six months ended June 30, 2021, time charter and voyage expenses were $3.9 million, or an average of $479 per day, compared to $6.2 million in the comparative period, or $762 per day, a decrease of $283 per ownership day, or 37.1%.

Depreciation and Amortization

Depreciation and amortization for the second quarter 2021 was $13.1 million, compared to $11.6 million in the second quarter of 2020. The increase in the amortization expense is due to the nine drydockings that have been completed since July 1, 2020. Depreciation was increased due to the acquisition of six vessels since April 1, 2021.

Depreciation for the six months ended June 30, 2021 was $25.5 million, compared to $23.1 million in the comparative period, with the increase being due to the addition of six vessels since July 1, 2020.

Gain on sale of vessel and impairment of vessels

The 2001-built, 2,272 TEU containership, La Tour, was sold on June 30, 2021 for net proceeds of $16.5 million resulting in a gain of $7.8 million. As of March 31, 2020, we had an expectation that the 1999-built, 2,200 TEU feeder ships, GSL Matisse and Utrillo, would be sold before the end of their previously estimated useful life, and as a result performed an impairment test of these two asset groups and an impairment charge of $7.6 million was recognized. An additional impairment charge of $0.9 million was recognized on these two vessels in the three months ended June 30, 2020 for a total of $8.5 million in the six month period ended June 30, 2020. The two vessels were sold in July 2020.

General and Administrative Expenses

General and administrative expenses were $1.9 million in the second quarter 2021, compared to $2.3 million in the second quarter of 2020. The decrease was mainly due to the non-cash effect of accelerated stock based compensation expense recognized in the second quarter of 2020. The average general and administrative expense per ownership day for the second quarter 2021 was $436, compared to $567 in the comparative period, a decrease of $131 or 23.1%.

For the six months ended June 30, 2021, general and administrative expenses were $6.1 million, compared to $4.8 million in the comparative period mainly due to the non-cash effect of accelerated stock based compensation expense recognized in the first quarter of 2021. The average general and administrative expense per ownership day for the six-month period ended June 30, 2021 was $755, compared to $587 in the comparative period, an increase of $168 or 28.6% mainly due to the non-cash effect of the accelerated stock based compensation expense.

Adjusted EBITDA

Adjusted EBITDA was $51.5 million for the second quarter 2021, up from $42.7 million for the second quarter of 2020, with the net increase being mainly due to the increased operating days and the addition of six vessels since July 1, 2020.

Adjusted EBITDA for the six months ended June 30, 2021 was $96.2 million, compared to $82.6 million for the comparative period, with the increase being due to the addition of six vessels since July 1, 2020.

Interest Expense and Interest Income

Debt as at June 30, 2021 totaled $835.4 million, comprising $684.2 million secured debt collateralized by our vessels, $68.7 million from sale and leaseback financing transactions and $82.5 million of unsecured indebtedness on our 2024 Notes. As of June 30, 2021, none of our vessels were unencumbered.

Debt as at June 30, 2020 totaled $845.0 million, comprising $267.0 million of indebtedness on our 2022 Notes and $4.7 million of indebtedness under a secured term loan, both cross collateralized by 18 vessels in the legacy GSL fleet, $59.0 million of unsecured indebtedness on our 2024 Notes, and $514.3 million other secured debt collateralized by our other vessels. As of June 30, 2020, five of our vessels were unencumbered.

Interest and other finance expenses for the second quarter 2021 were $14.0 million, a decrease of $2.0 million, or 12.5%, on the interest and other finance expenses for the second quarter of 2020 of $16.0 million. The decrease is mainly due to the full repayment of our expensive 2022 Notes in January 2021 and the partial repayment of our Blue Ocean Junior Credit Facility in February 2021 offset by the prepayment fee of $1.4 million paid in the second quarter on the repayment and completion of the refinancing of our Odyssia Credit Facilities and the interest on the new loan with HCOB and new sale and leaseback agreement with Neptune.

Interest and other finance expenses for the six months ended June 30, 2021 were $39.3 million, an increase of $3.8 million, or 10.7%, on the interest and other finance expenses for the comparative period, of $35.5 million. The increase is mainly due to $5.8 million premium paid on the redemption in full of our 2022 Notes in January 2021 compared to $2.3 million premium paid on the redemption $46.0 million of the 2022 Notes in March 2020 plus the acceleration of deferred financing charges of $3.7 million, and the acceleration of amortization of original issue discount associated with the redemption of the 2022 Notes of $1.1 million plus the prepayment fee of $1.6 million paid on the partial repayment of our Blue Ocean Junior Credit Facility, plus the prepayment fee of $1.4 million paid on the repayment and completion of the refinancing of our Odyssia Credit Facilities and the interest on a new loan with HCOB and a new sale and leaseback agreement with Neptune, offset by decrease in LIBOR.

Interest income for the second quarter 2021 was $0.1 million, compared to $0.2 million for the second quarter of 2020.

Interest income for the six months period ended June 30, 2021 was $0.3 million, compared to $0.8 million for the comparative period.

Other Income/(Expenses), Net

Other income, net was $0.6 million in the three months ended June 30, 2021, compared to an expense, net of $0.4 million in the second quarter of 2020.

Other income, net was $0.9 million in the six months period ended June 30, 2021, compared to an other expense, net of $0.4 million in the comparative period.

Taxation

Taxation for the three months ended June 30, 2021 was nil, compared to a credit of $3,000 in the second quarter of 2020.

Taxation for the six months ended June 30, 2021 was nil, compared to a credit of $3,000 in the six months ended June 30, 2020.

Earnings Allocated to Preferred Shares

Our Series B Preferred Shares carry a coupon of 8.75%, the cost of which for the second quarter 2021 was $2.0 million, compared to $0.9 million for the second quarter of 2020. The increase is due to additional Series B Preferred Shares issued under our ATM program since June 2020. The cost was $3.5 million in the six months ended June 30, 2021, compared to $1.8 million for the comparative period.

Net Income Available to Common Shareholders

Net income available to common shareholders for the three months ended June 30, 2021 was $30.1 million, including $7.8 million net gain on the sale of La Tour and the prepayment fee of $1.4 million on the completion of the refinancing of our Odyssia Credit Facilities. Net income available to common shareholders for the prior period was $12.6 million after $0.9 million impairment charges associated with the decision to dispose of GSL Matisse and Utrillo and $0.4 million for accelerated stock based compensation expense due to vesting.

Net income available to common shareholders for the six months ended June 30, 2021 was $34.2 million, after the $7.8 million net gain on the sale of La Tour, the prepayment fee of $1.6 million on the partial repayment of our Blue Ocean Junior Credit Facility, the prepayment fee of $1.4 million on the completion of the refinancing of our Odyssia Credit Facilities, the non-cash effect of $1.3 million for accelerated stock based compensation expense due to vesting and new awards of fully vested incentive shares, $5.8 million premium paid on the redemption in full of our 2022 Notes in January 2021, and associated accelerated amortization of $3.7 million deferred financing charges and $1.1 million original issue discount. Net income available to common shareholders for the prior period was $13.2 million after $8.5 million non-cash impairment charges associated with the decision to dispose of GSL Matisse and Utrillo, the non-cash effect of $0.4 million for accelerated stock based compensation expense due to vesting, and $2.3 million premium paid on the redemption of $46.0 million of our 2022 Notes in February 2020.

Normalized net income for the three months ended June 30, 2021, was $23.7 million, before the $7.8 million net gain on the sale of La Tour and the prepayment fee of $1.4 million paid on the repayment of our Deutsche, CIT, HCOB, Entrust Blue Ocean Credit Facility. Normalized net income for the three months ended June 30, 2020, was $13.9 million, before the $0.9 million impairment charges associated with the decision to dispose of GSL Matisse and Utrillo and $0.4 million for accelerated stock based compensation expense due to vesting.

Normalized net income for the six months period ended June 30, 2021 was $41.5 million before the $7.8 million net gain on the sale of La Tour, a prepayment fee of $1.6 million on the partial repayment of our Blue Ocean Junior Credit Facility, the prepayment fee of $1.4 million on the completion of the refinancing of our Odyssia Credit Facilities, the non-cash effect of $1.3 million for accelerated stock based compensation expense, $5.8 million premium paid on the redemption in full of our 2022 Notes in January 2021, and the associated accelerated amortization of $3.7 million deferred financing charges and $1.1 million original issue discount. Normalized net income in the comparative period was $24.4 million, before the $8.5 million non-cash impairment charges associated with the decision to dispose of GSL Matisse and Utrillo, the non-cash effect of $0.4 million for accelerated stock based compensation expense and $2.3 million premium paid on the redemption of $46.0 million of our 2022 Notes in February 2020.

Fleet

Our fleet comprises 65 containerships, of which – as at August 4, 2021 – four have yet to be delivered. The first table below presents the fleet prior to the vessel acquisitions announced year to date (the “Status Quo Fleet”); the second shows the 23 ships purchased and contracted to be purchased year to date (the “Purchased Fleet”).

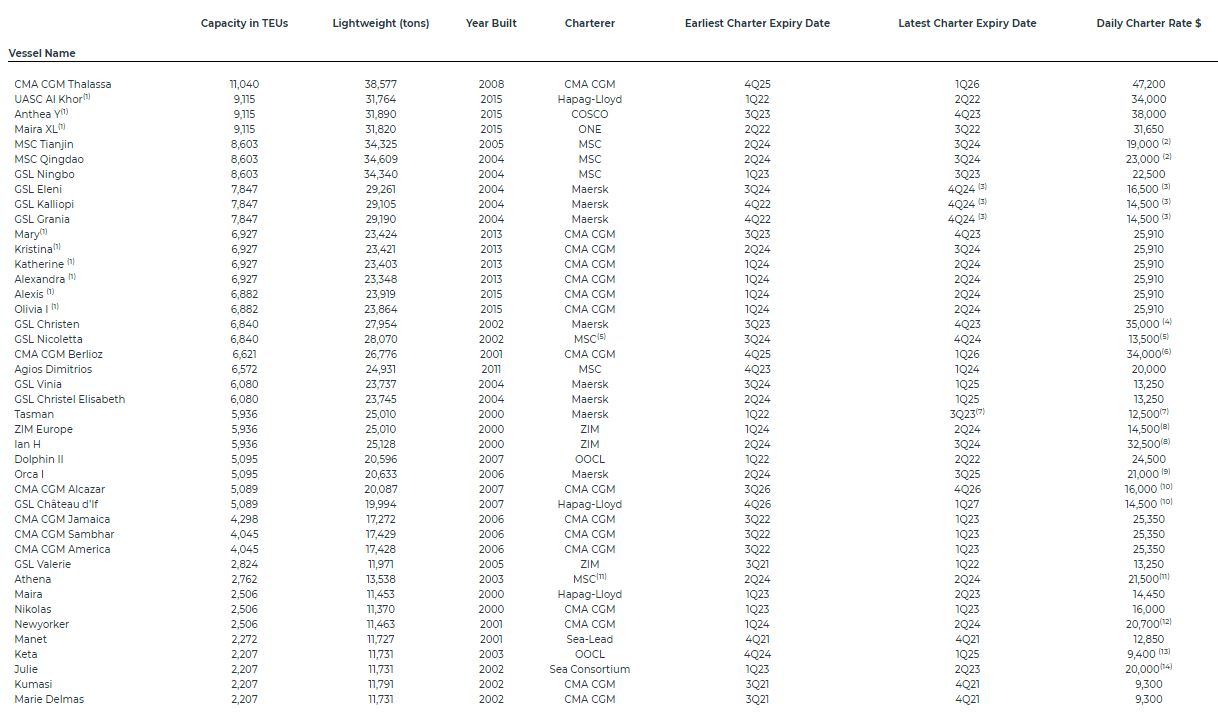

Status Quo Fleet

(1) Modern design, high reefer capacity, fuel-efficient vessel.

(2) MSC Tianjin. Chartered at $23,000 per day through dry-docking in 2Q2021; thereafter at $19,000 per day, due to cancellation of scrubber installation. MSC Qingdao has a scrubber installed and will continue to trade at a rate of $23,000 per day.

(3) GSL Eleni delivered 2Q2019 and is chartered for five years; GSL Kalliopi (delivered 4Q2019) and GSL Grania (delivered 3Q2019) are chartered for three years plus two successive periods of one year at the option of the charterer. During the option periods the charter rates for GSL Kalliopi and GSL Grania are $18,900 per day and $17,750 per day respectively.

(4) GSL Christen. Chartered at $15,000 per day through May 2021, at which time the rate increased to $35,000 per day.

(5) GSL Nicoletta. Chartered to MSC at $13,500 per day to 3Q21; thereafter to be chartered to Maersk at $35,750 per day.

(6) CMA CGM Berlioz. Chartered at $34,000 per day through December 2021, at which time the rate will increase to $37,750 per day.

(7) Tasman. 12-month extension at charterer’s option callable in 2Q2022, at an increased rate of $20,000 per day.

(8) A package agreement with ZIM, for direct charter extensions on two 5,900 TEU ships: Ian H, at a rate of $32,500 per day from May 2021, and ZIM Europe (formerly Dimitris Y), at a rate of $24,250 per day, from May 2022.

(9) Orca I. Chartered at $10,000 per day through April 2021, at which time the rate increased to $21,000 per day through to the median expiry of the charter in 2Q2024; thereafter the charterer has the option to charter the vessel for a further 12-14 months at the same rate.

(10) CMA CGM Alcazar and GSL Chateau d’If. Both ships have been forward fixed to CMA CGM for five years at $35,500 per day, with the new charters due to commence in 4Q2021;

(11) Athena. Chartered to MSC at a rate of $9,000 per day through April 2021, at which time the vessel was drydocked. Thereafter chartered to Hapag-Lloyd at $21,500 per day;

(12) Newyorker. Drydocked in 2Q2021; thereafter chartered to CMA CGM at $20,700 per day;

(13) Keta. Chartered to OOCL at $9,400 per day through 3Q2021. Thereafter forward fixed to CMA CGM at $25,000 per day;

(14) Julie. Chartered to Sea Consortium at a rate of $9,250 per day through May 2021; thereafter extended at $20,000 per day.

Purchased Fleet

(1) On February 9, 2021 we announced that we had contracted to purchase seven ships of approximately 6,000 TEU each, which have now been delivered. Contract cover for each vessel is for a firm period of at least three years from the date each vessel is delivered, with charterers holding a one-year extension option on each charter, followed by a second option with the period determined by (and terminating prior to) each vessel’s 25th year dry-docking & special survey. During the firm periods of cover the seven charters are expected to generate aggregate annualized Adjusted EBITDA of approximately $29.0 million. Five ships are chartered to Maersk from delivery; the remaining two (GSL Maria & GSL Violetta) will be chartered to Maersk upon completion of short charters to Wan Hai and ONE, respectively.

(2) On June 16, 2021 we announced that we had contracted to purchase four ultra-high reefer ships of 5,470 TEU each. These ships are scheduled to deliver in 3/4Q21. Contract cover is for a firm period of three years, with a period of an additional three years at charterers’ option. During the firm periods of cover the four charters are expected to generate aggregate annualized Adjusted EBITDA of approximately $31.1 million.

(3) GSL Eleftheria. Chartered to Maersk at $12,000 per day through September 2021; thereafter extended at $37,975 per day.

Source: Global Ship Lease