After a couple of weeks of mixed performances in steel plate prices from the sub-continent markets where the industry witnessed Indian levels suddenly jump towards the end of last week, whilst both Pakistani and Bangladeshi markets saw their plate prices decline, this week, the respective pendulums appear to be swinging back.

Bangladeshi plate prices finally steadied their recent month long decline through September, Pakistani plate made a small recovery and Indian levels plummeted nearly USD 25/Ton this week.

In the West, Turkey spent another quiet, yet steady week, even though Lira concerns are now starting to permeate through the local recycling mindset.

Supply too remains minimal and is possibly adding to the buoyancy of current vessel pricing in its own way. Accordingly, we continue to see either Cash Buyers concluding previously purchased tonnage, or news of private sales surface as this week, news of a tanker and bulker (for strictly HKC SoC green recycling) were concluded this week.

Local port positions also remain relatively full, with Chattogram (expectedly) claiming the highest volume of incoming tonnage in the subcontinent, for a few weeks now.

Meanwhile, GMS is pleased and proud to present an excellent Thought Leadership article published by Ms. Prachi Shah (In-house Legal, GMS Dubai) covering tanker contracts. We invite you to read it at https://www.hellenicshippingnews.com/tanking-contracts-doctrine-of-good-faith-versus-wog-and-other-exclusionary-terms/

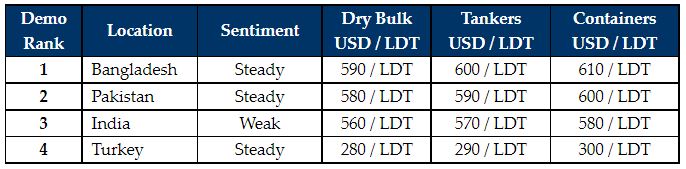

For week 41 of 2021, GMS demo rankings / pricing for the week are as below.

Source: GMS,Inc.