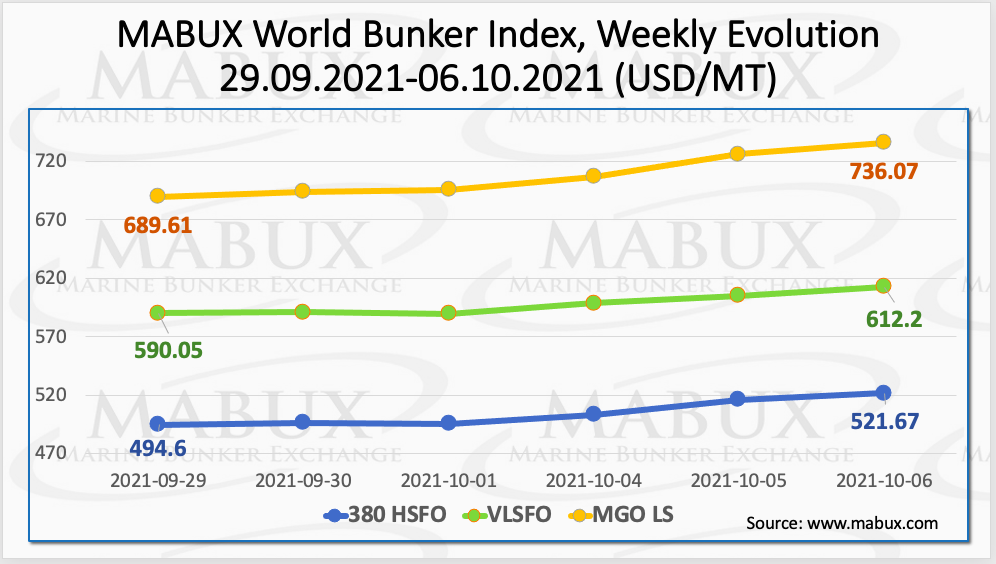

On a Week 40, the MABUX World Bunker Index continued its firm upward trend. The 380 HSFO index rose by 27.07 USD and overcame 500 USD mark: from 494.60 USD / MT to 521.67 USD / MT. The VLSFO index increased by 22.15 USD and exceeded the 600 USD mark: from 590.05 USD / MT to 612.20 USD / MT, while the MGO index added 46.46 USD and exceeded the 700 USD mark (from 689.61 USD / MT to 736.07 USD / MT). At the moment the average 380 HSFO and MGO LS world prices have fully regained the losses that took place in April-May 2020 and exceeded the price levels registered in early January 2020.

MABUX ARA LNG Bunker Index, calculated as the average price of LNG as a marine fuel in the ARA region, did not show any significant changes in the period from September 29 to October 06: a moderate decrease from 1046.11 USD / MT to 1039.31 USD / MT (minus 6.80 USD). The average LNG Bunker Index fell by 7.89 USD (1041.36 USD / MT versus 1049.24 USD / MT last week). The average MGO LS price in Rotterdam over the same period increased by 24.16 USD / MT, and the average price difference between bunker LNG and MGO LS in Rotterdam narrowed by 32.05 USD, breaking the 400 USD mark: (395.52 USD / MT versus 427.57 USD / MT last week). With an uncertain start of Nord Stream 2, gas prices in Europe continue to surge, also due to forecasts of cold weather in north Europe and lower production of electricity from nuclear generation in France, due to a strike. LNG bunker price indices are available in the LNG Bunkering section on www.mabux.com.

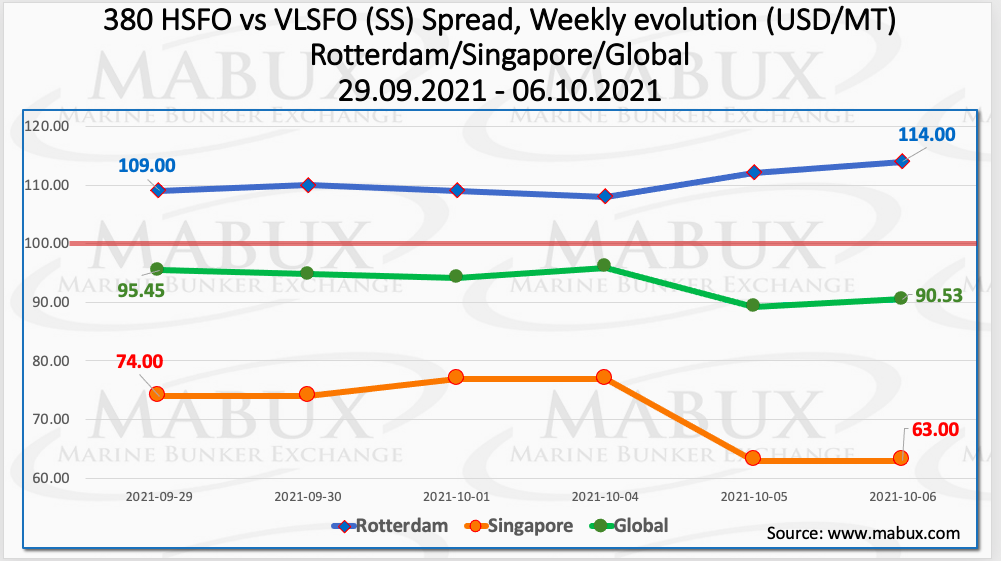

The average weekly Global Scrubber Spread (SS) – the difference in price between 380 HSFO and VLSFO – continued a slight decline during the week and amounted to $ 93.35 (versus $ 97.72 last week). Meantime, the average weekly SS Spread in Rotterdam widened slightly and remained stable above the $ 100 mark: $ 110.33 (against $ 108.33 last week, plus $ 2.00). The average SS Spread in Singapore, on the contrary, continued to decline and is well below the psychological mark of $ 100: $ 71.33 versus $ 77.67 last week (minus $ 6.34). More information is available in the Differentials section of www.mabux.com.

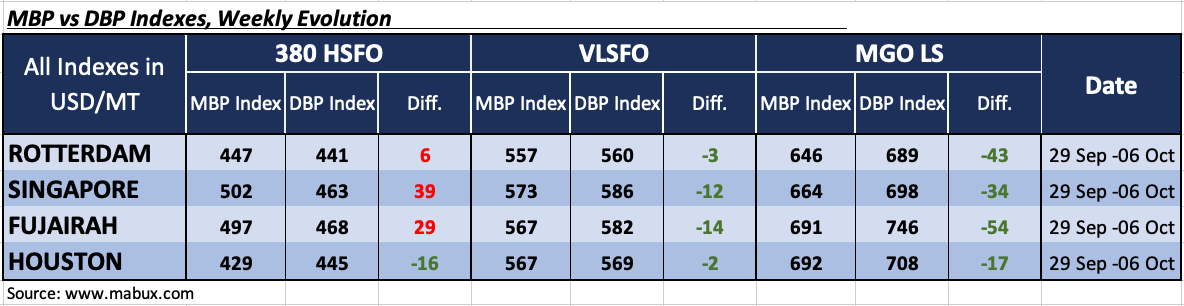

Correlation of MABUX MBP Index (Market Bunker Prices) vs MABUX DBP Index (MABUX Digital Benchmark) in the four global largest hubs over the past week showed that 380 HSFO fuel was overvalued in all selected ports, with the exception of Houston, where the Index recorded an underpricing of $ 16 (vs. minus $ 14 a week earlier). In other ports, 380 HSFO was overcharged: in Rotterdam – plus $ 6, in Singapore – plus $ 39 and in Fujairah – plus $ 29.

VLSFO fuel grade, according to the MABUX MBP / DBP Index, was in the undervaluation zone in all selected ports: in Rotterdam by minus $ 3, in Singapore by minus $ 12, in Fujairah by minus $ 14 and in Houston by minus $ 2.

The MABUX MBP / DBP Index also recorded an undercharge of MGO LS fuel at all selected ports: minimum value in Houston (minus $ 17), maximum value in Fujairah (minus $ 54).

Overall, 380 HSFO remains the only fuel type with overcharge status.

Pacific island countries calling on the International Maritime Organisation (IMO) to fully decarbonise the shipping industry by 2050, and to impose a US$100 carbon levy on shipping companies by 2025. The Climate Vulnerable Forum (CVF) held its fourth regional dialogue where eleven participating governments from Asia adopted an outcomes statement that backs proposals to clean up international shipping. The CVF is a grouping of around 50 of the most climate-threatened nations in the world, from Africa and the Middle East, Latin America and the Caribbean, Asia and the Pacific. Asia’s endorsement comes at the back of eight Pacific states throwing their support to the RMI, Kiribati and the Solomon Islands IMO proposals in September.

Source: www.mabux.com