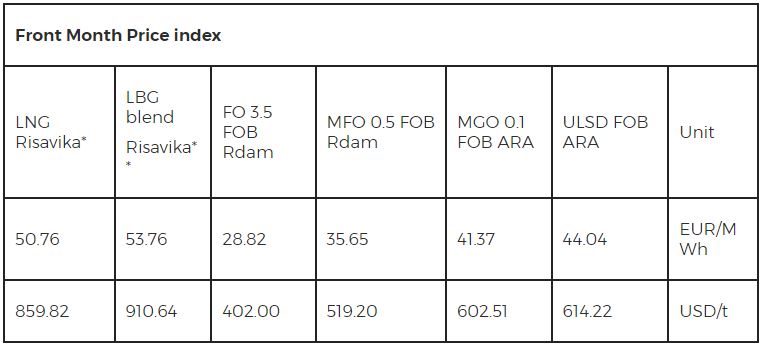

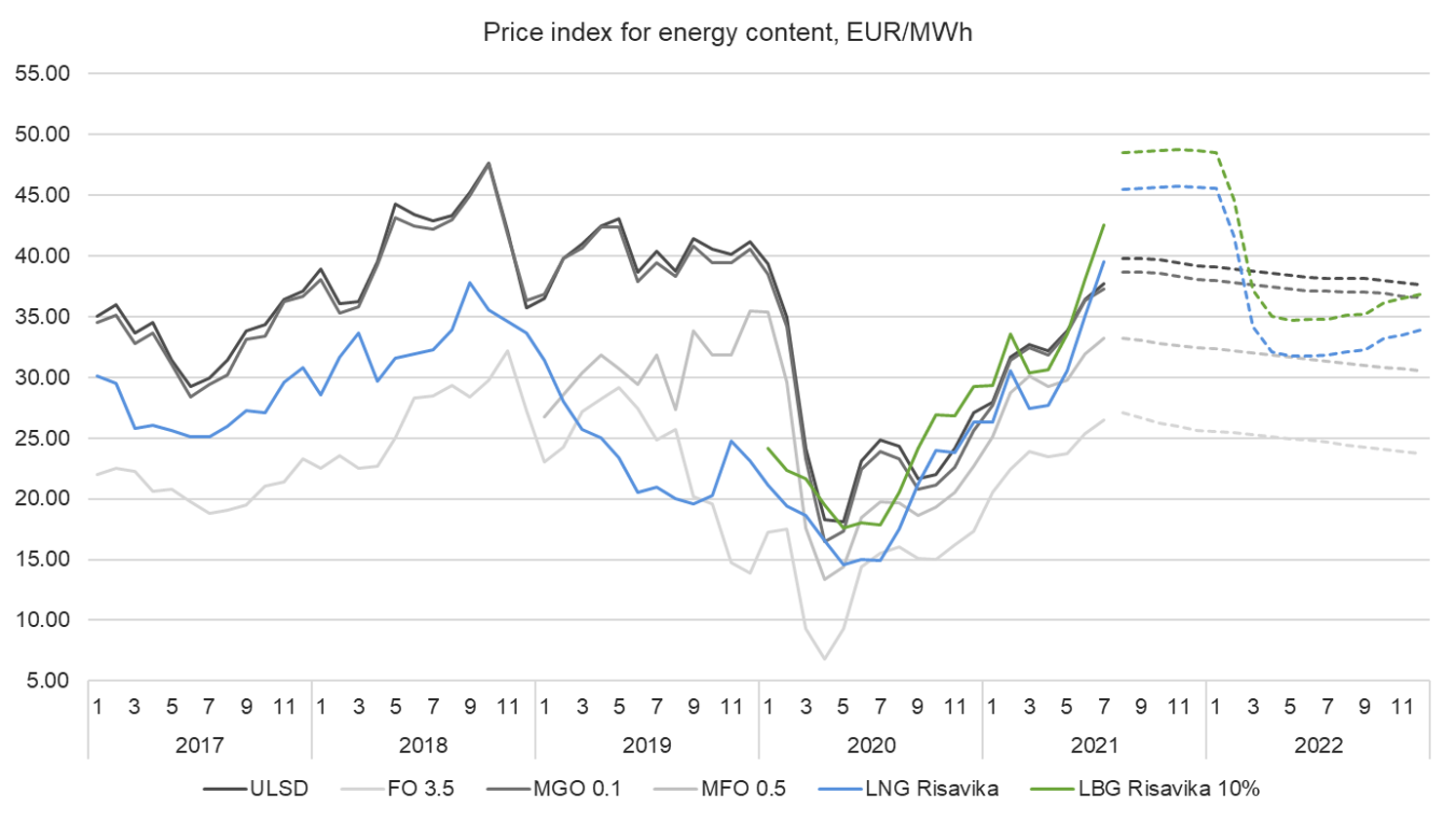

Risavika LNG index has increased to 50.76 EUR/MWh following the rally on the European gas markets prices for August contracts. The market continues its bullish trend. A severe tightening of the global LNG market resulted in a considerable drop in European imports during July, with seasonably low physical receipts falling by a further third both year on year and month on month. Although the spread has narrowed, Asian markets are still priced at premium leading to LNG cargoes diverting to that direction. This summer tight supply situation will have an impact also on winter prices as withdrawals from the storages would likely be priced higher than summer gas prices. The market is waiting for the start of Nord Stream 2 and increase in LNG availability, and already pricing it in as we see futures curve in a strong backwardation starting at the beginning of 2022.

Oil product prices were also up following benchmark crude prices last week. Fuel oil 3.5 (FO 3.5) price has gained 1.7 % and was at 402 USD/t, low sulphur oil (MFO 0.5) and marine gasoil (MGO 0.1) were up by 1.8 and 2.4 % to 519.2 USD/t and 602.51 USD/t respectively week on week. Oil market has been volatile, balancing between two main sentiments. Oil inventories draws indicate healthy demand and provide support, while spread of delta variant in Asia brings uncertainty on demand development especially considering oil production increase from OPEC+ members. Futures curves for oil products are also in backwardation, however, not as steep as for LNG.

LNG Risavika – LNG FOB Risavika

LBG Risavika 10 % – 10 % blend of Liquified Biogas

FO 3.5 FOB Rdam – European 3.5% Fuel Oil Barges FOB Rdam (Platts) Futures Quotes

MFO 0.5 FOB Rdam – European FOB Rdam Marine Fuel 0.5% Barges (Platts) Futures Quotes

MGO 0.1 FOB ARA – Gasoil 0.1% Barges FOB ARA (Platts) Futures Quotes

ULSD FOB ARA – European Diesel 10 ppm Barges FOB ARA (Platts) Futures Quotes

Source: Gasum