The latest stress test on Chinese banks shows that capital pressure on large and medium-sized banks is easing as the economy recovers from the pandemic, Fitch Ratings says. This supports our view earlier this year that the operating environment had improved, and our related decision to upgrade the Viability Ratings of China’s six state banks as well as some of the large joint stock commercial banks. However, small banks remain vulnerable due to their higher risk exposure and weaker capital buffers.

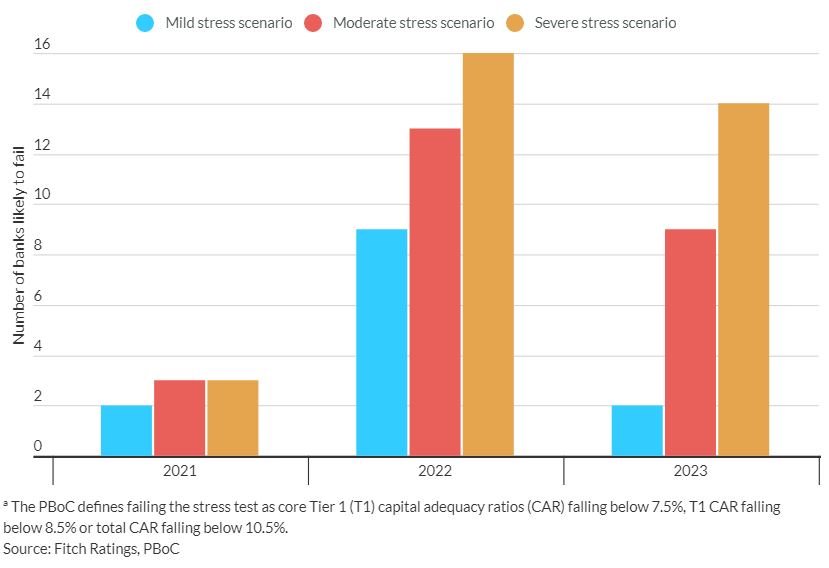

The stress-test results, released with the People Bank of China’s (PBoC) 2021 Financial Stability Report on 3 September, show that only three out of 30 large and medium-sized banks would fail to meet minimum regulatory capital requirements in 2021 under a severe economic slowdown. This is a significant improvement from last year, when 21 of the banks would have fallen below requirements in 2021 under the PBoC’s severe stress test, and nine would have fallen short under its moderate stress test.

The improved results reflect the economic recovery and the resolution of non-performing loans, as well as capital replenishment. We believe state banks and large joint stock commercial banks would continue to maintain capital well above the minimum requirements despite a probable economic slowdown from 2022. This is consistent with our view that the positive impact of the improved operating environment on banks’ Standalone Credit Profiles is greatest at the top end of the system.

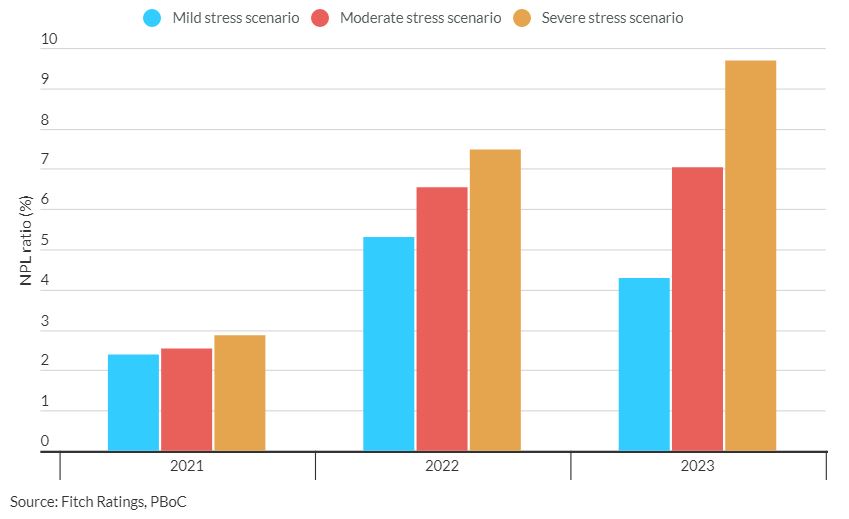

The PBoC’s mild stress uses real GDP growth at 7.3% in 2021 (2022: 4.8%; 2023: 4.1%), moderately below Fitch’s forecasts of 8.4% in 2021 (2022: 5.5%; 2023: 5.3%). Even under the mild stress, the results show a surge in non-performing loans (NPL) for the 30 large and medium-sized banks, with their NPL ratio increasing to 2.4% in 2021 (2022: 5.3%; 2023: 4.3%) from 1.8% at end-1H21.

The PBoC’s mild stress uses real GDP growth at 7.3% in 2021 (2022: 4.8%; 2023: 4.1%), moderately below Fitch’s forecasts of 8.4% in 2021 (2022: 5.5%; 2023: 5.3%). Even under the mild stress, the results show a surge in non-performing loans (NPL) for the 30 large and medium-sized banks, with their NPL ratio increasing to 2.4% in 2021 (2022: 5.3%; 2023: 4.3%) from 1.8% at end-1H21.

However, we expect ongoing resolution of NPLs to prevent such a sharp deterioration. There were CNY8.8 trillion NPLs resolved in 2017–2020 (CNY3.0 trillion in 2020), exceeding the combined total for the previous 12 years, and the authorities expect further increases in 2021 and 2022.

Unlike large and medium-sized banks, small banks still face significant capital pressure from economic slowdown and asset-quality risks. Small banks typically have higher risk appetites and weaker capital buffers as they have higher funding costs and weaker customer franchises. The PBoC’s sensitivity analysis shows that small banks’ capital ratios are typically much more sensitive to an increase in NPLs than those of larger banks. This supports our view that small banks benefit less from the broad operating environment improvement, and our related decision not to upgrade the Viability Ratings of some of the small joint stock commercial banks.

The PBoC says that increases in system leverage have moderated since 3Q20 and that leverage should be fairly stable from now on. Our own expectation of stabilising leverage was an important factor in our decision to raise our operating environment score for Chinese banks to ‘bbb-’/positive from ‘bb+’/stable in May 2021 (see Improved Operating Environment Credit Positive for China Banks).

We believe the PBoC’s broad commitment to contain system leverage and strengthen the regulatory framework for banks will lead to stronger capital buffers over time, particularly at weaker banks, helping to improve financial system stability and reduce contagion risks. The PBoC appears to be broadening its oversight of the financial system. This year’s stress test covered 4,015 banks, compared with about 1,500 banks previously, and the PBoC also included a contagion risk test in its 2021 stability report.

Source: Fitch Ratings